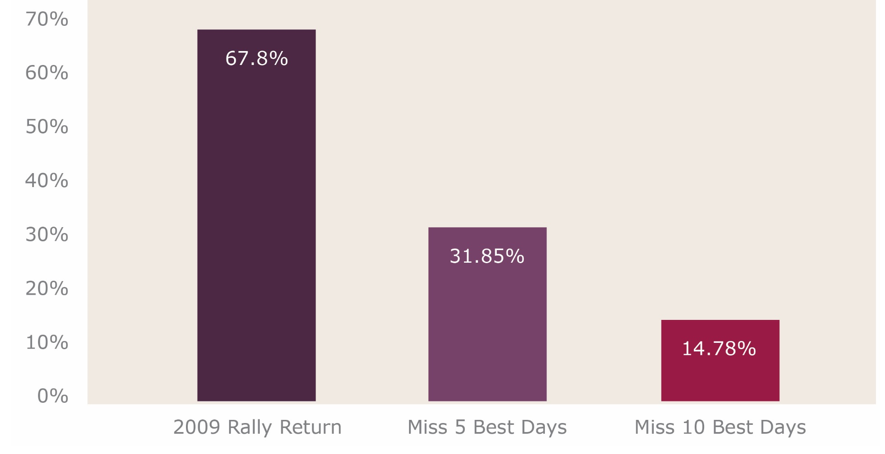

It is anything but business as usual in the U.S. and around the world today. With 1 in 3 Americans in lock down and most of the population trying to stay at home and practice social distancing, our wallets are shut not because we want them to be, but out of necessity for health reasons. Here are our most recent market commentary and thoughts on COVID-19 broken out into three categories: The Good, the Bad, and the Ugly. (You can find all of our commentary and resources on COVID-19 here). The Good Regardless of how you feel about government intervention and involvement, it is precisely in times like these that the Federal Government should intervene. The Federal Reserve announced over the weekend that it will provide “whatever it takes” to support the economy and the markets. They did not put a number on the amount of liquidity they will provide to keep the markets functioning properly. This is usually done with purchases of government bonds, but has now extended to municipal bonds and corporate bonds as well. The bond market had been seized up due to a lack of liquidity, and we believe this move will get things normalized sooner rather than later. This statement goes to show the Fed is very worried about the economy, and it should be. The Fed has taken aggressive action quickly rather than dragging its feet as it did in 2008. The amount of borrowing by the Fed (i.e., printing money) will be astronomical which will cause future challenges. However, given the urgency of the situation, the higher calling is alleviating problems now. South Korea showed that this pandemic can be successfully managed with a combination of widespread testing and quarantines. From a cultural and governing standpoint, our country will not have the ability to implement the degree of the lock-down that China or South Korea have done, but we can still avoid the fate of a country like Italy with the aggressive measures already underway. The lack of testing capabilities and resources available in the U.S. had been very disappointing, but in the last week, we’re starting to see a significant improvement. One week ago, we were conducting only just over 10,000 tests per day (3/16), but that number has risen to more than 60,000 tests per day one week later (as of 3/23). That is very encouraging because it means we’re getting enough data to start to know what we’re up against. The (Potentially) Bad Like the TARP (Troubled Asset Relief Program) vote all over again, the White House and the Senate has agreed upon a $2 Trillion dollar safety net program to help with the massive layoffs occurring now. It is absolutely necessary and we are relieved to learn that the two sides have come together to reach an agreement. This package has been compared to “business interruption insurance.” If it works effectively, it will provide money to businesses and individuals where losses have occurred due to no fault of their own. The goal of this massive economic relief package is to bridge the gap between now and normalization, by allowing struggling small businesses owners and individuals to sustain through this unprecedented period. The fate we are trying to avoid is a downward spiral for the economy. If unemployment gets out of control, personal spending and consumption will be cut way back, which would affect the health of companies which would lead to further cuts and more unemployment, and on it goes. That’s the reason why the performance of the equity markets so far this week has been linked so closely to the fate of this legislation. The Ugly The “ugly” part of this has to do with the headlines we expect to see going forward. We think the unemployment numbers could be staggering this next quarter, along with a significant decline in corporate earnings and profit. We have to be fully prepared for grave news reports about the spread of the contagion as well as the death rate. But while we believe the news will get worse from here, its ability to shock us will diminish. We believe a recession is a certainty at this point; the question is how deep it will be. Some of the economic numbers comparing March relative to February will look so bad they may seem like typos. The main question pertaining to the headlines is to what extent they are already priced-in to the markets. The thing to keep in mind is that the stock market moves ahead of the overall economy. So, for instance, when the market began a massive rally in 2009, the economy did not start to turn around until several months later. The recession officially ended in June 09 (three months after the market started a sharp rebound), but we did not even see substantial improvement in the economy for quite some time after. The economic news about the US economy was not getting better at the end of the financial crisis. But stocks stopped going down every time that bad news hit. It took a lot of pain to get to that point, but eventually, bad news fatigue had set in. This happened with regards to potential terror threats in the wake of 2001. And we fully expect it will happen again. A bear market like we’re experiencing is like pushing a beach ball underwater… When it starts to re-emerge, it doesn’t gradually drift upward, it pops up out of the water. The bottom of the market is not determined by extensive analysis; it’s more of a feeling that sets in. The news is still bad at that point when the recovery gets underway, but it’s ability to shock us is gone. Concluding Thoughts We'll continue to watch the current situation and look for opportunities to buy equities. But for now, we hope you feel confident about proactive planning we’ve done to help create a stronger plan for you and your family. It is exactly for times like these that we have developed the Retirement Shock Absorber® to help insulate your financial security from unforeseen events.

Market Commentary: The Good, the Bad & the Ugly